SMM reported on July 8:

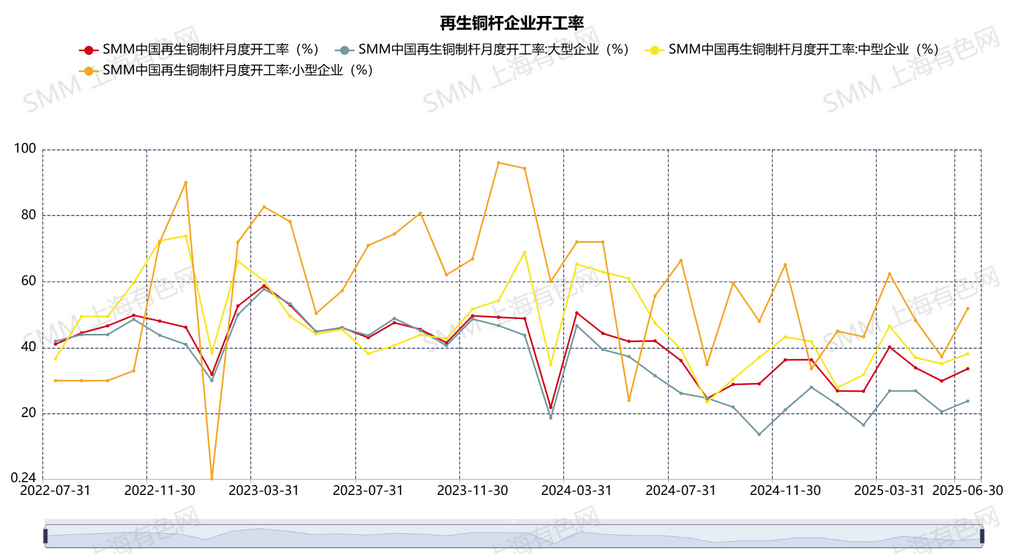

The operating rate of secondary copper rod enterprises in June was 33.61%, higher than the expected 30.84%, up 3.69% MoM, and down 8.44% YoY. The main theme surrounding secondary copper rod enterprises in June remained sales losses. According to SMM's statistical data from the gross profit theoretical model for secondary copper rod sales, secondary copper rod enterprises incurred an average sales loss of 410 yuan/mt in June, an increase of 165 yuan/mt MoM. The reason for this is that secondary copper rod enterprises, as part of the production and processing link in the industry chain, have been facing persistent tight supply of secondary copper raw materials. Imports of secondary copper raw materials in May saw a 9.55% MoM decline in volume.

Domestically, the heads of cargo yards in major distribution centers for secondary copper raw materials in China (such as Foshan, Guangdong, and Linyi, Shandong) stated that the regular inventory levels of secondary copper raw materials this year have only reached 50% of previous years' levels (for example, assuming a full warehouse of secondary copper raw materials is 100%, the current inventory level is only 20%-30%). Therefore, for most of June, the price of secondary copper raw materials followed the rise in copper prices. When prices fell, suppliers still refused to budge on prices or stopped shipping, resulting in artificially high prices for secondary copper raw materials.

On the consumption side, June and July are traditionally off-seasons in China. The operating rate of downstream wire and cable enterprises in June declined by 8.97% MoM. Weak end-use consumption has made it impossible for secondary copper rod enterprises to pass on the increased costs of raw material procurement to wire and cable enterprises. To ensure operations and control finished product inventories, secondary copper rod enterprises can only bear most of the sales losses themselves.

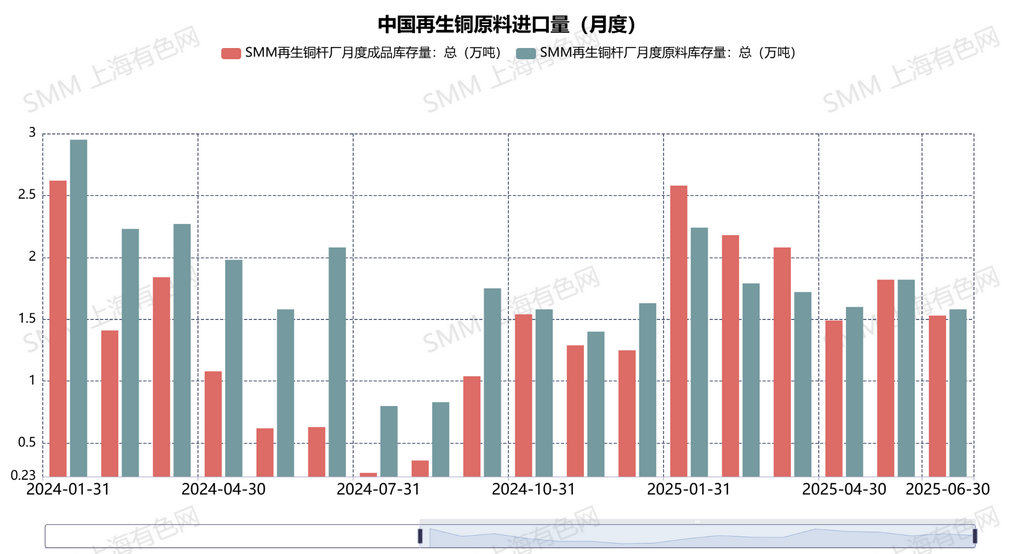

However, the reason for the counter-trend increase in the operating rate of secondary copper rod enterprises is that starting from mid-to-late June, domestic smelters temporarily halted external purchases of copper anodes due to mid-year inventory checks. As a result, many secondary copper rod enterprises had to switch their production lines back to producing secondary copper rods. According to the SMM survey, the finished product inventories of monthly sample enterprises for secondary copper rods were 15,300 mt, a decrease of 2,900 mt MoM. The average price difference between copper cathode rod and secondary copper rod in June was 1,193 yuan/mt, an increase of 43 yuan/mt MoM. The slight expansion of the price difference between copper cathode and copper scrap did not stimulate secondary copper rod consumption. The rise in copper prices near month-end further suppressed end-use consumption. Secondary copper rod enterprises reported that orders were more inclined towards traders. In summary, with the continuous shortage of raw materials and the off-season consumption, if secondary copper rod enterprises cannot convert their capacity to copper anodes, the number of operating days per week will further decrease from 4-5 days to 3 days.

The raw material inventory of secondary copper rod enterprises in June was 15,800 mt.

Whether imported or domestically produced, secondary copper raw materials remain in short supply. Sales losses persist for secondary copper rod enterprises. Under the situation where it is widely said among enterprises that "the more you produce, the more you lose," secondary copper rod enterprises are reluctant to purchase excessive amounts of secondary copper raw materials. This is to avoid inventory impairment losses caused by a decline in copper prices and to reduce the need for excessive reserves of secondary copper raw materials after slowing down the operating pace.

The operating rate of secondary copper rod is expected to be 29.4% in July.

In July, the operating rate of secondary copper rod enterprises will drop back slightly. Due to the continued difficulty in procuring high-grade secondary copper raw materials, secondary copper rod enterprises have reallocated their capacity to produce copper anodes. It is expected that the operating rate of secondary copper rod will decline by 4.21% MoM in July.